Position Size Calculator - R & ATR v1# Position Size Calculator - R & ATR

Professional position sizing tool for crypto traders using risk management principles and ATR-based stop loss placement.

## Features

✅ **Automatic ATR Calculation** - Uses ATR(14) by default, customizable period

✅ **Risk Management** - Calculate position size based on portfolio % risk

✅ **Tranche Support** - Split positions into multiple entries

✅ **Visual Stop Loss** - Red line showing stop loss placement on chart

✅ **Real-time Results** - Table displays all calculations instantly

✅ **Clean Interface** - Professional table with all key metrics

## How It Works

The indicator calculates optimal position size using this formula:

1. **Risk Amount** = Portfolio Size × (Risk % / 100)

2. **Stop Distance** = ATR × Multiplier

3. **Stop Loss Price** = Entry Price - Stop Distance

4. **Position Size** = Risk Amount / Stop Distance

5. **Tranche Size** = Position Size / Number of Tranches

## Settings

**Portfolio & Risk**

- Portfolio Size (USD): Your total trading capital

- Risk per Trade (R in %): Percentage of portfolio to risk per trade

- Number of Tranches: Split position into multiple entries

**ATR Settings**

- ATR Length: Period for ATR calculation (default: 14)

- ATR Multiplier: Multiply ATR for stop loss distance (0.5x, 1x, 1.5x, etc.)

**Display**

- Show Stop Loss Line: Toggle red stop loss line on chart

- Show Calculation Table: Toggle results table

## Results Displayed

- Risk Amount (1R): Dollar amount risked on trade

- Stop Distance: Distance from entry to stop loss

- Stop Loss: Exact stop loss price

- Risk per Coin: Amount risked per unit

- Position Size (coins): Number of coins to buy

"stop loss"に関するスクリプトを検索

Smart Money Concepts [XoRonX]# Smart Money Concepts (SMC) - Advanced Trading Indicator

## 📊 Deskripsi

**Smart Money Concepts ** adalah indicator trading komprehensif yang menggabungkan konsep Smart Money Trading dengan berbagai alat teknikal analisis modern. Indicator ini dirancang untuk membantu trader mengidentifikasi pergerakan institusional (smart money), struktur pasar, zona supply/demand, dan berbagai sinyal trading penting.

Indicator ini mengintegrasikan multiple timeframe analysis, order blocks detection, fair value gaps, fibonacci retracement, volume profile, RSI multi-timeframe, dan moving averages dalam satu platform yang powerful dan mudah digunakan.

---

## 🎯 Fitur Utama

### 1. **Smart Money Structure**

- **Internal Structure** - Struktur pasar jangka pendek untuk entry presisi

- **Swing Structure** - Struktur pasar jangka panjang untuk trend analysis

- **BOS (Break of Structure)** - Konfirmasi kelanjutan trend

- **CHoCH (Change of Character)** - Deteksi potensi reversal

### 2. **Order Blocks**

- **Internal Order Blocks** - Zona demand/supply jangka pendek

- **Swing Order Blocks** - Zona demand/supply jangka panjang

- Filter otomatis berdasarkan volatilitas (ATR/Range)

- Mitigation tracking (High/Low atau Close)

- Customizable display (jumlah order blocks yang ditampilkan)

### 3. **Equal Highs & Equal Lows (EQH/EQL)**

- Deteksi otomatis equal highs/lows

- Indikasi liquidity zones

- Threshold adjustment untuk sensitivitas

- Visual lines dan labels

### 4. **Fair Value Gaps (FVG)**

- Multi-timeframe FVG detection

- Auto threshold filtering

- Bullish & Bearish FVG boxes

- Extension control

- Color customization

### 5. **Premium & Discount Zones**

- Premium Zone (75-100% dari range)

- Equilibrium Zone (47.5-52.5% dari range)

- Discount Zone (0-25% dari range)

- Auto-update berdasarkan swing high/low

### 6. **Fibonacci Retracement**

- **Equilibrium to Discount** - Fib dari EQ ke discount zone

- **Equilibrium to Premium** - Fib dari EQ ke premium zone

- **Discount to Premium** - Fib full range

- Reverse option

- Show/hide lines

- Custom colors

### 7. **Volume Profile (VRVP)**

- Visible Range Volume Profile

- Point of Control (POC)

- Value Area (70% volume)

- Auto-adjust rows

- Placement options (Left/Right)

- Width customization

### 8. **RSI Multi-Timeframe**

- Monitor 3 timeframes sekaligus

- Overbought/Oversold signals

- Visual table display

- Color-coded signals (Red OB, Green OS)

- Customizable position & size

### 9. **Moving Averages**

- 3 Moving Average lines

- Pilihan tipe: EMA, SMA, WMA

- Automatic/Manual period mode

- Individual color & width settings

- Cross alerts (MA vs MA, Price vs MA)

### 10. **Multi-Timeframe Levels**

- Support up to 5 different timeframes

- Previous high/low levels

- Custom line styles

- Color customization

### 11. **Candle Color**

- Color candles berdasarkan trend

- Bullish = Green, Bearish = Red

- Optional toggle

---

## 🛠️ Cara Penggunaan

### **A. Setup Awal**

1. **Tambahkan Indicator ke Chart**

- Buka TradingView

- Klik "Indicators" → "My Scripts" atau paste code

- Pilih "Smart Money Concepts "

2. **Pilih Mode Display**

- **Historical**: Tampilkan semua struktur (untuk backtesting)

- **Present**: Hanya tampilkan struktur terbaru (clean chart)

3. **Pilih Style**

- **Colored**: Warna berbeda untuk bullish/bearish

- **Monochrome**: Tema warna abu-abu

---

### **B. Penggunaan Fitur**

#### **1. Smart Money Structure**

**Internal Structure (Real-time):**

- ✅ Aktifkan "Show Internal Structure"

- Pilih tampilan: All, BOS only, atau CHoCH only

- Gunakan untuk entry timing presisi

- Filter confluence untuk mengurangi noise

**Swing Structure:**

- ✅ Aktifkan "Show Swing Structure"

- Pilih tampilan struktur bullish/bearish

- Adjust "Swings Length" (default: 50)

- Gunakan untuk konfirmasi trend utama

**Tips:**

- BOS = Konfirmasi trend continuation

- CHoCH = Warning untuk possible reversal

- Tunggu price retest ke order block setelah BOS

---

#### **2. Order Blocks**

**Setup:**

- ✅ Aktifkan Internal/Swing Order Blocks

- Set jumlah blocks yang ditampil (1-20)

- Pilih filter: ATR atau Cumulative Mean Range

- Pilih mitigation: Close atau High/Low

**Cara Trading:**

1. Tunggu BOS/CHoCH terbentuk

2. Identifikasi order block terdekat

3. Wait for price pullback ke order block

4. Entry saat price respek order block (rejection)

5. Stop loss di bawah/atas order block

6. Target: swing high/low berikutnya

**Color Code:**

- 🔵 Light Blue = Internal Bullish OB

- 🔴 Light Red = Internal Bearish OB

- 🔵 Dark Blue = Swing Bullish OB

- 🔴 Dark Red = Swing Bearish OB

---

#### **3. Equal Highs/Lows (EQH/EQL)**

**Setup:**

- ✅ Aktifkan "Equal High/Low"

- Set "Bars Confirmation" (default: 3)

- Adjust threshold (0-0.5, default: 0.1)

**Interpretasi:**

- EQH = Liquidity di atas, kemungkinan sweep lalu dump

- EQL = Liquidity di bawah, kemungkinan sweep lalu pump

- Biasanya smart money akan grab liquidity sebelum move besar

**Trading Strategy:**

- Wait for EQH/EQL formation

- Anticipate liquidity grab

- Entry setelah sweep dengan konfirmasi (order block, FVG, CHoCH)

---

#### **4. Fair Value Gaps (FVG)**

**Setup:**

- ✅ Aktifkan "Fair Value Gaps"

- Pilih timeframe (default: chart timeframe)

- Enable/disable auto threshold

- Set extension bars

**Cara Trading:**

1. Bullish FVG = Support zone untuk buy

2. Bearish FVG = Resistance zone untuk sell

3. Price tends to fill FVG (retest)

4. Entry saat price kembali ke FVG

5. Partial fill = valid, full fill = invalidated

**Tips:**

- FVG + Order Block = High probability setup

- Multi-timeframe FVG lebih kuat

- Unfilled FVG = strong momentum

---

#### **5. Premium & Discount Zones**

**Setup:**

- ✅ Aktifkan "Premium/Discount Zones"

- Zones akan auto-update berdasarkan swing high/low

**Interpretasi:**

- 🟢 **Discount Zone** = Area BUY (price murah)

- ⚪ **Equilibrium** = Neutral (50%)

- 🔴 **Premium Zone** = Area SELL (price mahal)

**Trading Strategy:**

- BUY dari discount zone

- SELL dari premium zone

- Avoid trading di equilibrium

- Combine dengan structure confirmation

---

#### **6. Fibonacci Retracement**

**Setup:**

- Pilih Fib yang ingin ditampilkan:

- Equilibrium to Discount

- Equilibrium to Premium

- Discount to Premium

- Toggle show lines

- Enable reverse jika perlu

- Custom colors

**Key Levels:**

- 0.236 = Shallow retracement

- 0.382 = Common retracement

- 0.5 = 50% golden level

- 0.618 = Golden ratio (penting!)

- 0.786 = Deep retracement

**Cara Pakai:**

- 0.618-0.786 = Ideal entry zone dalam trend

- Combine dengan order blocks

- Wait for confirmation candle

---

#### **7. Volume Profile (VRVP)**

**Setup:**

- ✅ Aktifkan "Show Volume Profile"

- Set jumlah rows (10-100)

- Adjust width (5-50%)

- Pilih placement (Left/Right)

- Enable POC dan Value Area

**Interpretasi:**

- **POC (Point of Control)** = Harga dengan volume tertinggi = magnet

- **Value Area** = 70% volume = fair price range

- **Low Volume Nodes** = Weak support/resistance

- **High Volume Nodes** = Strong support/resistance

**Trading:**

- POC acts as support/resistance

- Price tends to return to POC

- Breakout dari Value Area = momentum

---

#### **8. RSI Multi-Timeframe**

**Setup:**

- ✅ Aktifkan "Show RSI Table"

- Set 3 timeframes (default: chart, 5m, 15m)

- Set RSI period (default: 14)

- Set Overbought level (default: 70)

- Set Oversold level (default: 30)

- Pilih posisi & ukuran table

**Interpretasi:**

- 🟢 **OS (Oversold)** = RSI ≤ 30 = Kondisi jenuh jual

- 🔴 **OB (Overbought)** = RSI ≥ 70 = Kondisi jenuh beli

- **-** = Neutral zone

**Trading Strategy:**

1. Multi-timeframe alignment = strong signal

2. OS + Bullish structure = BUY signal

3. OB + Bearish structure = SELL signal

4. Divergence RSI vs Price = reversal warning

**Contoh:**

- TF1: OS, TF2: OS, TF3: OS + Price di discount zone = STRONG BUY

---

#### **9. Moving Averages**

**Setup:**

- Pilih MA Type: EMA, SMA, atau WMA (berlaku untuk ketiga MA)

- Pilih Period Mode: Automatic atau Manual

- Set period untuk MA 1, 2, 3 (default: 20, 50, 100)

- Custom color & width per MA

- ✅ Enable Cross Alerts

**Interpretasi:**

- **Golden Cross** = MA fast cross above MA slow = Bullish

- **Death Cross** = MA fast cross below MA slow = Bearish

- Price above all MAs = Strong uptrend

- Price below all MAs = Strong downtrend

**Trading Strategy:**

1. MA1 (20) = Short-term trend

2. MA2 (50) = Medium-term trend

3. MA3 (100) = Long-term trend

**Entry Signals:**

- Price bounce dari MA dalam trend = continuation

- MA cross dengan konfirmasi structure = entry

- Multiple MA confluence = strong support/resistance

**Alerts Available:**

- MA1 cross MA2/MA3

- MA2 cross MA3

- Price cross any MA

---

#### **10. Multi-Timeframe Levels**

**Setup:**

- Enable HTF Level 1-5

- Set timeframes (contoh: 5m, 1H, 4H, D, W)

- Pilih line style (solid/dashed/dotted)

- Custom colors

**Cara Pakai:**

- Previous high/low dari HTF = strong S/R

- Breakout HTF level = significant move

- Multiple HTF levels confluence = major zone

---

### **C. Trading Setup Combination**

#### **Setup 1: High Probability Buy (Bullish)**

1. ✅ Swing structure: Bullish BOS

2. ✅ Price di Discount Zone

3. ✅ Pullback ke Bullish Order Block

4. ✅ Bullish FVG di bawah

5. ✅ RSI Multi-TF: Oversold

6. ✅ Price bounce dari MA

7. ✅ POC/Value Area support

8. ✅ Fibonacci 0.618-0.786 retracement

**Entry:** Saat price reject dari order block dengan confirmation candle

**Stop Loss:** Below order block

**Target:** Swing high atau premium zone

---

#### **Setup 2: High Probability Sell (Bearish)**

1. ✅ Swing structure: Bearish BOS

2. ✅ Price di Premium Zone

3. ✅ Pullback ke Bearish Order Block

4. ✅ Bearish FVG di atas

5. ✅ RSI Multi-TF: Overbought

6. ✅ Price reject dari MA

7. ✅ POC/Value Area resistance

8. ✅ Fibonacci 0.618-0.786 retracement

**Entry:** Saat price reject dari order block dengan confirmation candle

**Stop Loss:** Above order block

**Target:** Swing low atau discount zone

---

#### **Setup 3: Liquidity Grab (EQH/EQL)**

1. ✅ Identifikasi EQH atau EQL

2. ✅ Wait for liquidity sweep

3. ✅ Konfirmasi dengan CHoCH

4. ✅ Order block terbentuk setelah sweep

5. ✅ Entry saat retest order block

---

### **D. Tips & Best Practices**

**Risk Management:**

- Selalu gunakan stop loss

- Risk 1-2% per trade

- Risk:Reward minimum 1:2

- Jangan over-leverage

**Confluence adalah Kunci:**

- Minimal 3-4 konfirmasi sebelum entry

- Lebih banyak konfirmasi = higher probability

- Quality over quantity

**Timeframe Analysis:**

- HTF (Higher Timeframe) = Trend direction

- LTF (Lower Timeframe) = Entry timing

- Align dengan HTF trend

**Backtesting:**

- Gunakan mode "Historical"

- Test strategy di berbagai market condition

- Record dan analyze hasil

**Market Condition:**

- Trending market = Follow BOS, use order blocks

- Ranging market = Use premium/discount zones, EQH/EQL

- High volatility = Wider stops, wait for clear structure

**Avoid:**

- Trading di equilibrium zone

- Entry tanpa konfirmasi

- Fighting the trend

- Overleveraging

- Emotional trading

---

## 📈 Recommended Settings

### **For Scalping (1m - 5m):**

- Internal Structure: ON

- Swing Structure: OFF

- Order Blocks: Internal only

- RSI Timeframes: 1m, 5m, 15m

- MA Periods: 9, 21, 50

### **For Day Trading (15m - 1H):**

- Internal Structure: ON

- Swing Structure: ON

- Order Blocks: Both

- RSI Timeframes: 15m, 1H, 4H

- MA Periods: 20, 50, 100

### **For Swing Trading (4H - D):**

- Internal Structure: OFF

- Swing Structure: ON

- Order Blocks: Swing only

- RSI Timeframes: 4H, D, W

- MA Periods: 20, 50, 200

---

## ⚠️ Disclaimer

Indicator ini adalah alat bantu analisis teknikal. Tidak ada indicator yang 100% akurat. Selalu:

- Lakukan analisa fundamental

- Gunakan proper risk management

- Praktik di demo account terlebih dahulu

- Trading memiliki resiko, trade at your own risk

---

## 📝 Version Info

**Version:** 5.0

**Platform:** TradingView Pine Script v5

**Author:** XoRonX

**Max Labels:** 500

**Max Lines:** 500

**Max Boxes:** 500

---

## 🔄 Updates & Support

Untuk update, bug reports, atau pertanyaan:

- Check documentation regularly

- Test new features in replay mode

- Backup your settings before updates

---

## 🎓 Learning Resources

**Recommended Study:**

1. Smart Money Concepts (SMC) basics

2. Order blocks theory

3. Liquidity concepts

4. ICT (Inner Circle Trader) concepts

5. Volume profile analysis

6. Multi-timeframe analysis

**Practice:**

- Start with higher timeframes

- Master one concept at a time

- Keep a trading journal

- Review your trades weekly

---

**Happy Trading! 🚀📊**

_Remember: The best indicator is your own analysis and discipline._

Strong Candle and Probability Levels Light [SYNC & TRADE]Indicator Description: "Strong Candle and Probability Levels Light "

Core Philosophy: This indicator is not just a collection of random signals. It is a complete trading system built around two core concepts: Strength (Volume-based Candles) and Probability (Fibonacci Levels), synchronized between spot and futures markets to filter out noise and manipulations.

🎯 The "Strong Candle Defense" Strategy

The primary tactic is to enter in the direction of the market's dominant force at an optimal price.

1. Identifying Strength: The indicator identifies "Strong Candles" in real-time — candles with anomalously high volume and significant delta (buyer/seller dominance), confirmed across multiple timeframes. They are marked with circles (blue for bullish, red for bearish) and Z-level labels showing the statistical significance of the move.

2. "Ladder" Entry: We do not chase the market. The strategy is to wait for a pullback (retest) to the body of the strong candle or its key internal Fibonacci levels (38.2%, 50%, 61.8%) for a favorable entry. The position is built in parts ("scaling in") as the bounce is confirmed.

3. Profit-Taking Targets: The main take-profit targets are set at the external Fibonacci extension levels:

First Target: 161.8% — The classic level to secure the first portion of profits.

Second Target: 261.8% (or 227% in Light mode) — The level for capturing extended moves, where the remaining position is exited.

Refined Stop-Loss Rules and Strategy Invalidation Conditions:

Primary Stop-Loss: Placed beyond the extreme of the strong candle (the Fibonacci grid's 0% level). For a long position — below the strong candle's low; for a short position — above its high.

Strategy Invalidation Criterion: The strategy is considered invalidated, and the position should be exited, if the price closes a candle's body beyond the key protective level. This specifically means:

For a Long: A candle closes (the close price) below the low of the strong candle.

For a Short: A candle closes (the close price) above the high of the strong candle.

This criterion, especially on lower timeframes, provides a stricter and more timely signal of a setup failure than a mere wick break.

Alternative Supertrend Stop-Loss: The proprietary Supertrend line can be used as a dynamic trailing stop. The stop-loss is placed behind the Supertrend line, and a candle close beyond this line also signals a trend violation and the need to exit the position.

📊 Unique Automated Fibonacci Grids

Our Fibonacci grids are not the standard, static drawing tool. They are a dynamic profit-taking and management system.

Automatic Plotting: A new grid is automatically drawn on every new strong candle, freeing the trader from manual work.

Smart Management:

Self-Cleaning: When enabled, the grid automatically removes itself after the price has fully "filled" its range (reached the 0% level), preventing chart clutter.

Dynamic Levels: Depending on the selected type (Fibonacci Light, Standard, Extended, Geometric), a different set of internal and external levels is plotted, adapting the tool to various trading styles from scalping to position trading.

Key Difference from Standard Tools: Unlike the basic Fibonacci tool, our grids are an integral part of the trading logic. They are tied to strong candles (high-probability points), update automatically, and act as an execution system for the strategy, not just an analysis tool.

📈 Proprietary Supertrend with Advanced Filtering

We do not use the standard, off-the-shelf Supertrend. Our version is a hybrid algorithm, supercharged with volume analysis.

Dynamic ATR Multiplier: The indicator's multiplier adapts to market conditions. During high volume delta (strong buying/selling pressure), the multiplier increases, making the trend line less sensitive and helping you stay in the trade during strong impulses.

Strong Candle Filter: Supertrend signal changes can be optionally restricted to confirm only on strong candles. This drastically reduces false entries. The trend doesn't change just based on volatility (ATR), but upon confirmation by real strength (volume).

Profit Potential: Combining signals from this filtered Supertrend with the "Strong Candle Defense" strategy allows for precise entry timing in the direction of the major trend, with clear and statistically sound profit targets.

⚙️ Additional Systems for Enhanced Accuracy

Spot & Futures Sync: The indicator compares strength between spot and futures markets. A divergence (e.g., a strong long candle on spot but weakness on futures) is marked as a potential "Manipulation" (X), warning you of an unreliable signal.

Multi-Timeframe Volume Analysis: Delta and volume are analyzed from lower timeframes, providing a more granular picture within a single candle of your current TF.

Supertrend Table: A quick overview of the trend direction across all major timeframes (from 5m to 1W) in a single table.

Conclusion:

The "Strong Candle and Probability Levels Light" indicator is a professional suite for traders who want to trade not just signals, but probabilities. The strategy, built around defending strong candles, combined with unique automated Fibonacci grids and an adaptive Supertrend, provides a clear plan from entry to exit. The use of market synchronization and multi-timeframe volume analysis minimizes noise and false signals, allowing you to focus on high-quality setups.

Turtle Long & Short (Donchian + N-Stop). Overview and Core Functionality

The indicator implements the classic Turtle Trading System rules. It uses two sets of Donchian Channels for generating entry and exit signals, and the Average True Range (ATR), referred to as N, to calculate a dynamic, volatility-adjusted initial stop-loss.

The script simulates a position's life cycle (entry, holding the fixed initial stop, and exiting) and only conditionally displays the calculated initial stop-loss price on the chart when a trade signal is active.

2. Key Input Parameters (Adjustable Settings)

The script provides detailed input groups for customization:

A. Signal Settings:

len_entry (Default: 20): Period for the Entry Donchian Channel (20-day high/low breakout).

len_exit (Default: 10): Period for the Exit Donchian Channel (10-day low/high trailing stop).

B. Risk Settings (N):

len_atr (Default: 20): Period used to calculate the Average True Range (N), which determines volatility.

stop_loss_multiplier (Default: 2.0): The factor applied to N to calculate the initial stop-loss (e.g., 2.0×N=2N).

C. Label Display: Controls the appearance of the entry labels.

label_background_color_long / label_background_color_short: Background color for Long/Short entry labels.

label_text_color: Text color for the labels.

label_size_input: Size control for the label (tiny, small, normal, large, huge).

3. Trading Logic and State Management

A. Entry and Exit Conditions

Trade Type Entry Condition Trailing Exit Condition Stop-Loss (SL)

Long Close > 20-period High Close < 10-period Low Fixed Entry Price−(Multiplier×N)

Short Close < 20-period Low Close > 10-period High Fixed Entry Price+(Multiplier×N)

In Google Sheets exportieren

B. Position State Management

The script uses persistent var float variables (fixed_long_stop_price and fixed_short_stop_price) to maintain the state:

Upon an Entry signal, the calculated stop-loss price is fixed and assigned to the respective var variable.

The variable holds this fixed price on subsequent bars.

The price is reset to na (Not Applicable) only when an Exit condition (10-period trailing exit, fixed stop-loss hit, or reverse entry signal) is met.

This logic ensures the initial stop-loss line is plotted only when a simulated trade is active.

4. Visual Elements and Alerts

Donchian Channels: Plotted as two lines (Entry High/Exit Low) with a fill for visualization.

N-Stop-Loss Lines: Two lines (fixed_long_stop_price in Fuchsia and fixed_short_stop_price in Orange) are plotted using plot.style_linebr, ensuring they appear only after a trade signal fires and disappear on exit.

Signal Shapes (plotshape):

Long Entry: Green triangle below the bar.

Short Entry: Red triangle above the bar.

Long/Short Exits: Diamond shapes indicating the trailing stop exit.

Entry Labels (label.new): Custom-colored labels appear at the point of entry, displaying the current N value and the exact calculated N-Stop price.

Alerts (alertcondition): Alerts are set up for both Long Entry and Short Entry conditions.

Cumulative Delta_Effort vs Result_immy**Cumulative Delta Oscillator\_effort**

This script creates a “Cumulative Delta Effort vs Result” oscillator, a custom indicator designed to measure the balance between buying and selling pressure (Effort) versus actual price movement (Result).

**How It Works**

Delta Volume: Measures aggressive buying vs selling per candle.

Cumulative Delta: Tracks net buying/selling pressure over time.

Effort vs Result: Compares volume delta (effort) to price movement (result).

Oscillator: Highlights divergence between effort and result, useful for spotting absorption (high effort, low result) and exhaustion (low effort, high result).

Histogram: Visual cue for accumulation/distribution zones.

----------------------------

This indicator combines volume delta (effort) and price movement (result), so it tells you how efficiently volume is moving price — a concept sometimes called effort vs. result analysis in Wyckoff or volume–spread analysis (VSA).

🔍 Concept Summary

Effort (delta volume) = how much buying/selling pressure is there (volume side).

Result (price change) = how much that effort moves price (price side).

Oscillator (Effort − Result) = how much “extra” effort is not producing movement — often showing absorption or exhaustion.

📈 How to Interpret the Signals

1\. Oscillator above Signal line → Bullish Momentum

When osc > signal, histogram turns green.

Means buying effort is stronger than price reaction — often early sign of accumulation or rising demand.

This can signal:

Possible bullish continuation if confirmed by rising prices.

Or early absorption if prices aren’t yet breaking out (smart money absorbing supply).

✅ Bullish Entry Signal:

When the oscillator crosses above the signal line (green cross) and price is near support or consolidating → potential long setup.

2\. Oscillator below Signal line → Bearish Momentum

When osc < signal, histogram turns red.

Selling effort dominates; can mean increasing supply or price exhaustion.

This often appears before:

Bearish continuation (trend strengthening)

Or upthrust/exhaustion (price rising on weak volume)

❌ Bearish Entry Signal:

When the oscillator crosses below the signal line (red cross), especially if near resistance → potential short setup.

3\. Crossovers

The alert is triggered when: ta.cross(osc, signal)

That means:

Bullish crossover: oscillator line crosses above signal → potential buy momentum shift.

Bearish crossover: oscillator line crosses below signal → potential sell momentum shift.

These work like MACD crossovers, but volume-adjusted.

4\. Zero Line

The zero line is the neutral point.

When osc crosses above zero, overall buying effort exceeds price change — market gaining strength.

When osc crosses below zero, selling pressure increases — market weakening.

→ Combining signal line crosses with zero-line crosses gives stronger confirmation.

5\. Histogram Analysis (Absorption \& Exhaustion)**

Tall green bars: rising momentum (buyers dominate)

Tall red bars: falling momentum (sellers dominate)

Shrinking bars: momentum fading — possible reversal zone.

If volume increases but price stalls, oscillator may spike while price stays flat — absorption (big players taking the opposite side).

If price surges but oscillator weakens, exhaustion — move running out of volume support.

------------------------------------------------------------------------

🧠 Practical Strategy Example

Situation What It Might Mean Possible Action

Oscillator crosses above signal near support Buyer effort increasing, price may rise Go long / close shorts

Oscillator crosses below signal near resistance Seller effort rising, price may drop Go short / take profits

Oscillator high but price flat Absorption (big players absorbing supply) Wait for breakout confirmation

Oscillator low but price flat Absorption (demand absorbing supply) Look for bullish reversal

Oscillator diverges from price Volume–price divergence Early warning of reversal

⚙️ Best Practice

Works best on volume-sensitive assets (futures, crypto, forex tick data).

**Combine with:**

Price structure (support/resistance)

Volume profile / delta footprint

Candle confirmation

We’ll go through both bullish and bearish examples so you can see how to trade with it in real market context.

---------------------------------------------------------------------------------

🟩 Example 1 — Bullish Setup (Long Trade)

Step 1. Context: Identify Potential Support Zone

Before relying on any indicator, find support using:

Previous swing low

Demand zone

VWAP / volume profile node

Trendline or moving average

👉 You’re looking for a place where buyers might step in.

Step 2. Wait for Oscillator Signal

Watch the oscillator panel:

The oscillator (green line) has been below the signal line (orange) → bearish phase.

Then it crosses above the signal line and the histogram turns green.

This means:

➡️ Buying “effort” is increasing faster than price reaction — momentum shift upward.

Step 3. Confirm with Price

On your chart:

Candle closes above short-term resistance or above previous candle high

Ideally volume confirms (green candle with increasing volume)

✅ Bullish Entry Condition

osc crosses above signal

price closes above local resistance

Step 4. Entry \& Stop

Entry: Next candle open after confirmation cross

Stop-loss: Below recent swing low or support zone

Take profit:

2R or 3R target

or near next resistance level

🧠 Optional filter: Only take the trade if oscillator is rising from below zero (coming out of weakness).

Step 5. Manage Trade

If oscillator flattens or starts curling down → tighten stop

If it crosses below the signal again → consider exit

Example Interpretation:

Oscillator crosses above signal from -200 to +100, histogram turns green, price breaks a resistance line → strong bullish reversal → enter long.

🟥 Example 2 — Bearish Setup (Short Trade)

Step 1. Context: Find Resistance

Look for: Prior swing high

Supply zone

Major moving average

Trendline top

Step 2. Wait for Oscillator Cross Down

The oscillator (green) crosses below the signal line (orange).

Histogram turns red.

This means:

➡️ Selling effort is rising relative to price movement — bearish pressure.

Step 3. Confirm with Price

Price fails to make higher highs, or

Forms a bearish engulfing candle near resistance.

✅ Bearish Entry Condition

osc crosses below signal

price confirms with bearish candle

Step 4. Entry \& Stop

Entry: On next candle open

Stop-loss: Above resistance or recent swing high

Take profit: 2R or more or at next major support

Step 5. Exit on Opposite Signal

If oscillator crosses back above signal → momentum shift → exit short.

⚙️ Pro Tips

Tip Why It Matters

Use on 15m–4H+ charts More reliable delta signal

Combine with volume or OBV Confirms “effort” strength

Watch divergences Early reversals

Align with higher timeframe trend Avoid countertrend traps

-------------------------------------------------------------------------------------------------

🧩 Quick Checklist

Step Condition Action

1 Identify zone (support/resistance) Mark area

2 Oscillator crossover Prepare order

3 Candle confirmation Enter

4 Stop-loss \& target Manage risk

5 Opposite cross Exit

Please follow and like if you appreciate my work. thank you.

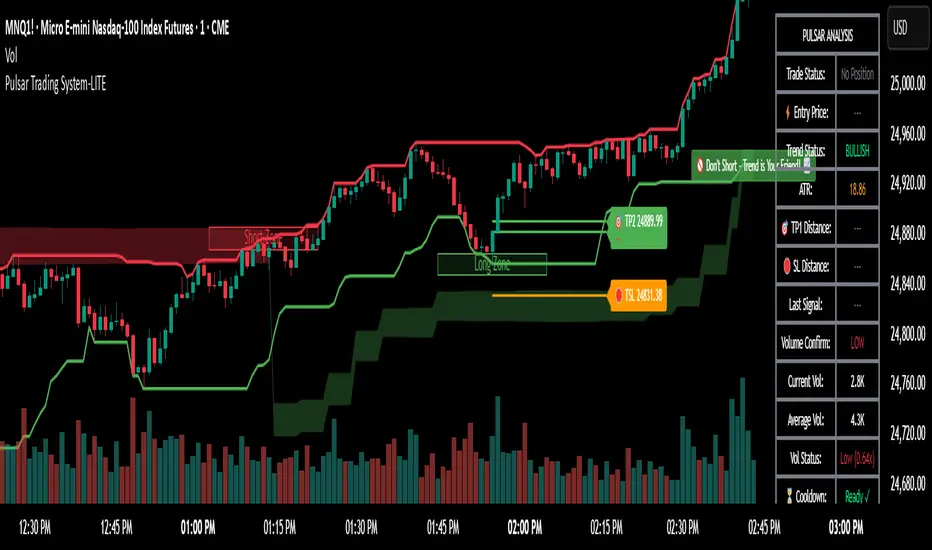

Pulsar Trading System-LITE📡 Pulsar Trading System

OVERVIEW

Pulsar is a comprehensive breakout trading system that combines dynamic support/resistance detection, trend filtering, and volume confirmation to identify high-probability entry opportunities. Unlike simple breakout indicators, Pulsar uses multi-timeframe analysis and adaptive ATR-based calculations to filter false signals and provide complete trade management from entry to exit.

WHAT MAKES THIS ORIGINAL

This indicator is unique in its integration of multiple complementary systems:

-Adaptive ATR Zones: Support and resistance levels are not static—they dynamically adjust based on current market volatility (ATR), creating entry zones that expand and contract with market conditions rather than using fixed price levels.

-Multi-Timeframe SuperTrend Filter: The trend filter operates on a higher timeframe than the chart (e.g., 5-minute SuperTrend on a 1-minute chart) to prevent counter-trend trades while maintaining granular entry precision. The visual ribbon with humorous warning text ("🚫 Don't Short - Trend is Your Friend! 📈") provides immediate trend awareness.

-Intelligent Cooldown System: After any trade exit (stop loss or take profit), the system enters a configurable cooldown period, preventing overtrading during choppy or consolidating market conditions—a critical feature often missing in breakout systems.

-Dynamic Trailing Stops: The trailing stop uses ATR multipliers to lock in profits while adapting to volatility, moving only in the favorable direction and never loosening.

-Comprehensive Dashboard: Real-time analysis displays trade status, entry prices, distances to targets in both points and ATR multiples, volume confirmation status, and cooldown countdown.

HOW IT WORKS

Core Detection Logic:

Pulsar identifies breakout opportunities by monitoring price interaction with dynamically calculated support and resistance levels:

Support/Resistance Calculation: Uses ta.lowest() and ta.highest() over a configurable lookback period to identify key levels, then adds ATR-based buffers (0.5 × ATR) to create entry zones.

Breakout Conditions:

Long Entry: Price closes above support buffer AND recent low touched support AND volume exceeds threshold

Short Entry: Price closes below resistance buffer AND recent high touched resistance AND volume exceeds threshold

SuperTrend Filter: A separate higher-timeframe SuperTrend calculation determines overall trend direction. Entries only trigger when breakout direction aligns with SuperTrend (bullish breakout + bullish trend, or bearish breakout + bearish trend).

Volume Confirmation: Current volume must exceed a configurable multiple of the 14-period SMA (default 1.0×) to confirm genuine interest in the breakout.

Cooldown Mechanism: After exit, the system tracks bars elapsed and blocks new signals until the cooldown period completes, preventing rapid-fire entries in ranging markets.

Trade Management:

Stop Loss: Calculated as entry zone ± (ATR × SL Multiplier)

Take Profit 1: Entry zone ± (ATR × TP1 Multiplier)

Take Profit 2: Entry zone ± (ATR × TP2 Multiplier)

Trailing Stop (optional): Updates every bar, moving the stop closer by maintaining distance of (ATR × Trailing Multiplier) from current price, but only in favorable direction

SuperTrend Calculation:

The SuperTrend uses standard methodology:

Upper Band = (High + Low) / 2 + (Multiplier × ATR)

Lower Band = (High + Low) / 2 - (Multiplier × ATR)

Direction changes when price crosses opposite band

The ribbon visualization adds a width offset (ATR × Ribbon Width) to create a filled zone rather than a single line.

HOW TO USE

Setup:

Add Pulsar to your chart (works best on liquid instruments like NQ, ES, CL)

Configure timeframe-specific settings (see recommendations below)

Enable SuperTrend Filter for trend-following mode, or disable for pure breakout mode

Set up alerts for Entry, TP1, TP2, and Stop Loss events

Recommended Settings by Timeframe:

1-Minute Charts:

Lookback Period: 10-15

SuperTrend Timeframe: 5 min

ATR Timeframe: 5 min (for stability)

Cooldown: 8-12 bars

Trailing Stop: Enabled with 0.8-1.0 multiplier

5-Minute Charts:

Lookback Period: 15-20

SuperTrend Timeframe: 15 min

ATR Timeframe: current chart

Cooldown: 5-8 bars

Trailing Stop: Optional

15-Minute+ Charts:

Lookback Period: 20-30

SuperTrend Timeframe: 1 hour

ATR Timeframe: current chart

Cooldown: 3-5 bars

Trailing Stop: Optional

Interpreting Signals:

Long/Short Zone Box: Green (long) or red (short) box appears when breakout conditions are met

Blue Entry Line: Shows your entry price

Red/Orange SL Line: Red = fixed stop, Orange = trailing stop (moves in real-time)

Green TP Lines: TP1 (closer) and TP2 (further) targets

SuperTrend Ribbon: Green = bullish trend (favor longs), Red = bearish trend (favor shorts)

Dashboard Status: Monitor trade state, distances, volume confirmation, and cooldown

Best Practices:

Use SuperTrend Filter: Significantly reduces false signals by avoiding counter-trend trades

Enable Cooldown on Fast Timeframes: Prevents overtrading on 1-5 minute charts

Volume Confirmation is Critical: Don't lower volume multiplier below 0.9 on futures

Use Higher Timeframe ATR: On 1-minute charts, use 5-minute ATR for stability

Avoid Major News Events: Disable during FOMC, NFP, CPI releases

Scale Out Strategy: Consider taking partial profits at TP1, letting remainder run to TP2

Parameter Optimization:

Start conservative and adjust based on results:

Too many stop-outs: Increase SL multiplier or SuperTrend multiplier

Missing good trades: Decrease volume multiplier or cooldown period

Too many false signals: Increase volume multiplier, lookback period, or cooldown

Profits not protected: Enable trailing stop or reduce trailing multiplier

KEY FEATURES

✅ Dynamic ATR-Based Zones: Entry, stop loss, and take profit levels automatically adjust to market volatility

✅ Multi-Timeframe Trend Filter: Uses higher timeframe SuperTrend to eliminate counter-trend trades

✅ Volume Confirmation: Filters low-volume false breakouts

✅ Intelligent Cooldown: Prevents overtrading with configurable post-trade waiting period

✅ Trailing Stop System: Optional dynamic stops that lock in profits using ATR distance

✅ Real-Time Dashboard: 13-row analysis showing trade status, targets, distances, volume, and cooldown

✅ Visual Ribbon Warnings: Humorous trend-following reminders on SuperTrend ribbon

✅ Complete Alert System: Notifications for entries, TP1, TP2, fixed stops, and trailing stops

✅ Customizable Visuals: Adjustable colors, dashboard position, text size, and line lengths

✅ Non-Repainting: Uses lookahead = barmerge.lookahead_off for all multi-timeframe calculations

SETTINGS EXPLAINED

SuperTrend Filter:

Enable: Toggle trend filtering on/off

Timeframe: Higher timeframe for trend analysis (recommended 3-5x chart timeframe)

ATR Period: Period for ATR calculation in SuperTrend (10-14 standard)

Multiplier: Distance from center band (2.5-3.5 for most markets)

Ribbon Width: Visual thickness of trend ribbon (0.2-0.5)

Core Parameters:

Lookback Period: Bars used to identify support/resistance (lower = more sensitive)

ATR Period: Bars for Average True Range calculation (14 is standard)

ATR Timeframe: Use higher timeframe ATR for smoother calculations on fast charts

Volume Multiplier: Required volume vs average (1.0 = average, 1.5 = 50% above average)

TP/SL:

SL Multiplier: Stop loss distance in ATR units (1.0-2.0 typical)

TP1 Multiplier: First target in ATR units (1.5-2.5 typical)

TP2 Multiplier: Second target in ATR units (2.0-3.5 typical)

Trailing Stop:

Enable: Activate dynamic trailing stop

Multiplier: Distance from current price in ATR units (0.8-1.5 typical)

Cooldown:

Enable: Prevent new signals after trade exit

Bars: Number of bars to wait before allowing next trade (higher on fast timeframes)

IMPORTANT NOTES

⚠️ Not a Holy Grail: No indicator is perfect. Pulsar is a tool that requires proper risk management, position sizing, and trading discipline.

⚠️ Backtest First: Test settings on historical data before live trading. Results vary by instrument, timeframe, and market conditions.

⚠️ Market Conditions Matter: Breakout systems perform best in trending markets. Consider reducing size or disabling during known choppy periods.

⚠️ Stop Loss is Mandatory: Always use the provided stop loss levels. Markets can move against you rapidly.

⚠️ Volume Data Required: This indicator requires volume data to function properly. It will display a warning if volume is unavailable.

⚠️ No Repainting: All multi-timeframe calls use non-repainting settings. What you see in real-time is what will be plotted historically.

TECHNICAL SPECIFICATIONS

Version: Pine Script v6

Type: Indicator (overlay = true)

Max Boxes: 500 (for zone visualization)

Max Lines: 500 (for TP/SL levels)

Max Labels: Unlimited (for annotations)

Repainting: None (uses lookahead = barmerge.lookahead_off)

COMPATIBLE INSTRUMENTS

Works best on liquid instruments with reliable volume data:

✅ Futures: NQ, MNQ, ES, MES, YM, MYM, RTY, M2K, CL, GC

✅ Forex: Major pairs (EUR/USD, GBP/USD, etc.)

✅ Stocks: Large-cap stocks with high volume

⚠️ Crypto: Works but requires higher ATR multipliers

❌ Low Volume Stocks: May produce unreliable signals

SUPPORT

For questions, suggestions, or to report issues, please comment below. I actively maintain this indicator and appreciate feedback from the community.

Enjoy trading with Pulsar! 🌟

Smart Liquidity & OTE Analysis Tool # Smart Liquidity & OTE Analysis Tool

## OVERVIEW

This indicator is designed for traders who utilize institutional trading concepts, specifically liquidity sweeps and optimal trade entry (OTE) zones, combined with session-based market structure analysis. It identifies potential market manipulation points where stop losses are likely clustered, and highlights high-probability entry zones based on Fibonacci retracements.

The tool combines four main analytical components that work synergistically to identify trading opportunities aligned with smart money behavior.

---

## CORE CONCEPTS & METHODOLOGY

### 1. TRADING SESSIONS ANALYSIS

**What it does:**

The indicator tracks three major forex trading sessions with customizable time zones:

- **Asian Session** (Default: 01:00-13:00 UTC+4) - Typically characterized by range-bound price action

- **London Session** (Default: 11:00-20:00 UTC+4) - High volatility period with increased institutional activity

- **New York Session** (Default: 17:00-00:00 UTC+4) - Overlaps with London creating peak liquidity

**How it works:**

- Automatically highlights active sessions with colored background boxes

- Draws session high/low lines which often act as intraday support/resistance

- Identifies session overlaps (e.g., London-NY overlap) where volatility and liquidity are highest

- Color-codes the price bars during overlaps to alert traders to increased opportunity periods

- Displays real-time session status (🟢 Open / 🔴 Closed) for quick reference

**Trading Application:**

Session highs and lows frequently become liquidity targets. The indicator helps traders anticipate when price might sweep these levels before continuing in the original direction. Session overlaps are prime times for major moves as multiple institutional players are active simultaneously.

---

### 2. EXTERNAL LIQUIDITY SWEEPS

**What it does:**

Identifies when price "sweeps" or breaks beyond significant swing highs and lows where stop losses are typically clustered. These sweeps often precede reversals or continuations after liquidity is collected.

**How it works:**

- Scans the previous 20 bars (configurable) to identify swing high and low points

- Marks these levels as "buyside liquidity" (above highs) or "sellside liquidity" (below lows)

- Monitors price action using three detection methods:

* **Wick Break:** Any candle wick extending beyond the liquidity level

* **Close Break:** Candle body closing beyond the level (stronger confirmation)

* **Full Retrace:** Price breaks the level then closes back inside the range (classic liquidity grab)

- Uses an ATR-based buffer to avoid false signals from minor price spikes

- Confirms sweeps only after a configurable number of confirmation bars to reduce repainting

**The Logic Behind It:**

Institutional traders need liquidity to fill large orders. Stop losses clustered above swing highs and below swing lows provide this liquidity. When these levels are swept, it often indicates smart money is entering positions in the opposite direction, causing reversals.

**Visual Representation:**

- Blue horizontal lines mark buyside liquidity zones (above price)

- Gray horizontal lines mark sellside liquidity zones (below price)

- Labels indicate when liquidity has been swept (✓) or remains active

- Historical zones are maintained for context (configurable display limit)

---

### 3. INTERNAL LIQUIDITY DETECTION

**What it does:**

Identifies equal highs (EQH) and equal lows (EQL) within recent price action - levels that have been tested multiple times without breaking. These represent internal liquidity pools that price often revisits before making larger moves.

**How it works:**

- Examines the most recent 8 bars (configurable) for price levels that occur multiple times

- Uses an ATR-based threshold (default 0.1% of ATR) to determine if highs or lows are "equal"

- Requires minimum 3 occurrences (configurable) of the same level to qualify as internal liquidity

- Tracks both the creation and sweeping of these internal levels

- Differentiates between wick breaks and close breaks for sweep confirmation

**The Concept:**

Unlike external liquidity at swing points, internal liquidity represents recent stop clusters and pending orders within the current price structure. Identifying these levels helps traders anticipate short-term price targets and potential reversal points before larger directional moves.

**Why This Matters:**

Price often needs to clear internal liquidity before making sustained moves to external liquidity levels. This creates a "roadmap" of where price is likely to go in sequence, improving trade timing.

**Visual Representation:**

- Cyan lines mark internal buyside liquidity (equal highs)

- Orange lines mark internal sellside liquidity (equal lows)

- Dashed or solid lines based on user preference

- Labels show when internal levels are swept

---

### 4. OPTIMAL TRADE ENTRY (OTE) ZONES

**What it does:**

Calculates and displays Fibonacci retracement zones (0.618-0.786) from recent swing points, representing "discount" or "premium" areas where institutional traders often enter positions after a liquidity sweep or structure break.

**How it works:**

- Identifies swing highs and lows using a 10-bar lookback period (configurable)

- Calculates three key Fibonacci levels:

* **0.618** - The "golden ratio" retracement (most significant)

* **0.705** - Mid-point between 0.618 and 0.786

* **0.786** - Deep retracement level (square root of 0.618)

- Optionally requires a structure break before displaying OTE zones

- Dynamically extends zones as new price action develops

- Tracks whether price has entered the zone (✅) or exited without filling (❌)

- Displays up to 2 most recent zones (configurable) to avoid chart clutter

**The Methodology:**

OTE zones represent areas where price is at a "discount" (for longs) or "premium" (for shorts) relative to the recent swing. After a liquidity sweep or structure break, institutional traders often wait for retracements into these zones before entering, as it offers better risk-to-reward ratios.

**Combining with Liquidity:**

The most powerful setups occur when:

1. External liquidity is swept

2. Price retraces into an OTE zone

3. Internal liquidity is present as a target

This confluence suggests smart money activity and high-probability trade opportunities.

**Visual Representation:**

- Shaded blue zone between 0.618 and 0.786 levels

- Three horizontal lines showing key Fibonacci levels with different colors/styles

- Labels (🎯) indicate bullish or bearish OTE zones

- Entry (✅) and exit (❌) status for each zone

---

## WHY THESE FEATURES WORK TOGETHER

This indicator combines these four components because they represent different stages of institutional trading behavior:

1. **Session Timing** - Identifies WHEN institutional activity is highest

2. **Liquidity Sweeps** - Shows WHERE smart money is collecting liquidity

3. **OTE Zones** - Highlights WHERE institutional entries likely occur after sweeps

4. **Internal Liquidity** - Provides SHORT-TERM targets for profit-taking or add-ons

Rather than using each concept in isolation, this integration creates a complete market structure framework. For example:

- A buyside liquidity sweep during London open →

- Followed by a retrace into a bullish OTE zone →

- With internal sellside liquidity as the initial target

This sequence represents a complete high-probability trade setup aligned with smart money principles.

---

## ANTI-REPAINTING FEATURES

**The Repainting Problem:**

Many indicators that identify patterns on historical data repaint their signals when live trading, showing signals that weren't actually there in real-time. This creates a false sense of accuracy.

**Our Solution:**

- **Confirmation Bars Setting:** Signals only appear after X bars have confirmed the pattern (default: 2 bars)

- **Marked Confirmation:** Labels show "C" when using confirmed signals

- **Trade-off:** More confirmation = less repainting but slightly delayed signals

- **User Control:** Traders can toggle between real-time signals (faster but may repaint) and confirmed signals (delayed but reliable)

---

## KEY CUSTOMIZATION OPTIONS

### Master Controls

- Toggle each major feature on/off independently

- Combine only the features relevant to your trading style

### Display Settings

- Adjust lookback periods for each component

- Control number of historical zones displayed

- Customize colors, line styles, and transparency

- Show/hide labels and session names

- Configure text sizes for different screen setups

### Detection Sensitivity

- **Sweep Detection:** Choose between wick breaks, close breaks, or full retraces

- **ATR Buffer:** Add distance requirements to confirm sweeps (reduces false signals)

- **Equal Level Threshold:** Adjust how close levels must be to qualify as "equal"

- **Confirmation Bars:** Balance between signal speed and reliability

### Alert System

- Session open/close notifications

- Liquidity sweep alerts

- OTE zone entry alerts

- Configurable alert frequency and types

---

## HOW TO USE THIS INDICATOR

### Basic Setup

1. Add the indicator to your chart (works on all timeframes, though 5M-1H recommended for intraday)

2. Enable the features you want to use via Master Controls

3. Adjust colors and transparency to match your chart preferences

4. Configure alert preferences if using notifications

### Trading Workflow

**Step 1: Identify the Session**

- Determine which trading session is active or approaching

- Note session highs/lows as potential liquidity targets

- Be especially alert during session overlaps

**Step 2: Watch for Liquidity Sweeps**

- Monitor external liquidity lines (swing highs/lows)

- When price sweeps liquidity, anticipate a potential reversal

- Stronger sweeps (close breaks + full retraces) are more significant

**Step 3: Wait for OTE Retracement**

- After a sweep, wait for price to retrace into the OTE zone (0.618-0.786)

- Bullish OTE after sellside sweep = potential long

- Bearish OTE after buyside sweep = potential short

**Step 4: Use Internal Liquidity as Targets**

- Look for internal liquidity in the direction of your trade

- These serve as initial profit targets

- External liquidity serves as extended targets

**Step 5: Manage Confirmation Settings**

- For live trading, use confirmed signals (2+ confirmation bars)

- For backtesting or analysis, you may use real-time signals

- Note that confirmed signals appear with "C" marking

### Example Trade Scenarios

**Bullish Setup:**

1. London session opens (increased volume)

2. Price sweeps sellside liquidity below Asian low

3. Price retraces into bullish OTE zone (0.618-0.786 of the sweep move)

4. Target internal buyside liquidity, then external buyside liquidity

**Bearish Setup:**

1. NY session overlap with London (peak liquidity)

2. Price sweeps buyside liquidity above recent high

3. Price retraces into bearish OTE zone

4. Target internal sellside liquidity, then session lows

---

## BEST PRACTICES

### What This Indicator Does Well

✓ Identifies high-probability institutional trading zones

✓ Provides clear visual roadmap of likely price targets

✓ Reduces chart clutter with configurable history limits

✓ Works across multiple timeframes and instruments

✓ Minimizes repainting with confirmation settings

### What This Indicator Doesn't Do

✗ Does not provide entry/exit arrows (intentional - requires trader discretion)

✗ Does not guarantee winning trades (no indicator does)

✗ Does not work in isolation (combine with price action/market context)

✗ Does not replace risk management (always use stop losses)

### Recommended Complementary Analysis

- Price action patterns (engulfing candles, pinbars at OTE zones)

- Volume profile or footprint charts for order flow confirmation

- Higher timeframe trend context (don't fade strong trends)

- Economic calendar awareness (avoid major news events)

---

## TECHNICAL NOTES

### Performance Optimization

- Uses max_bars_back limitation to reduce memory usage

- Automatic cleanup of old zones to prevent slowdown

- Efficient array management with configurable display limits

- Suitable for both intraday and swing trading timeframes

### Timeframe Recommendations

- **1-5 Minute:** Scalping with tight internal liquidity targets

- **15-30 Minute:** Intraday trading with session-based setups

- **1-4 Hour:** Swing trading with multi-session analysis

- **Daily:** Position trading using weekly liquidity levels

### Instrument Compatibility

Works on all liquid instruments:

- Forex pairs (optimal due to clear sessions)

- Stock index futures (ES, NQ, etc.)

- Cryptocurrency (24/7 markets - use custom session times)

- Individual stocks (less pronounced session effects)

---

## EDUCATIONAL RESOURCES

To better understand the concepts used in this indicator:

**Liquidity Concepts:**

- Study institutional order flow and stop loss hunting

- Learn about market microstructure and liquidity provision

- Understand the difference between retail and institutional trading

**Fibonacci/OTE:**

- Research Fibonacci retracements in trending markets

- Study the mathematical significance of the golden ratio (0.618)

- Practice identifying retracement entries on historical charts

**Session Trading:**

- Analyze volume profiles during different forex sessions

- Study typical price behavior during session overlaps

- Understand timezone conversions for your local trading hours

---

## VERSION HISTORY & UPDATES

This script represents a complete integration of multiple smart money concepts into a single, cohesive tool. Future updates will be published using the Update feature rather than creating separate scripts for minor variations.

---

## DISCLAIMER

This indicator is for educational and informational purposes only. It does not constitute financial advice or trading recommendations. All trading involves risk, and past performance does not guarantee future results. Always practice proper risk management and never risk more than you can afford to lose.

The concepts presented here (liquidity sweeps, OTE zones, session analysis) are widely discussed trading theories. This indicator is an interpretation and visualization of these concepts, not a guarantee of their effectiveness.

---

## SETTINGS SUMMARY

**Master Controls:** Enable/disable each major feature independently

**Repainting Controls:** Adjust confirmation requirements for signals

**Trading Sessions:** Customize session times, colors, and display options

**External Liquidity:** Configure detection sensitivity and visual styling

**Internal Liquidity:** Adjust lookback periods and threshold sensitivity

**OTE Zones:** Select which Fibonacci levels to display and entry requirements

**Alerts:** Configure notifications for sessions, sweeps, and entries

---

## SUPPORT & FEEDBACK

If you find this indicator helpful, please leave a like and comment with your feedback. For questions about specific settings or concepts, refer to the tooltips in the indicator settings panel - each parameter includes a detailed explanation.

Remember: The best indicator is the one you understand and can apply consistently within your trading plan. Take time to practice with this tool on demo accounts before risking real capital.

量价策略信号+K线pinbar+波动率出场+市场结构【梦喂马】v3Part 1: Indicator Module Explained (Code Analysis and Function Description)

Module 1: Master Switches

This is your "dashboard master control." Due to the numerous indicator functions, charts can appear cluttered. Here, you can easily turn each major function module on or off, allowing you to focus on the information you need most.

- Suggested Usage: When using it for the first time, you can start by only turning on the Vegas Channel and Core Entry Signals to familiarize yourself with the system's main trend judgment and entry logic. Then gradually turn on other modules to experience how they work together.

Module 2: Core Entry Signals (Long/Short Signals)

This is the "engine" of the entire system, responsible for generating the highest quality trend-following trading signals. The appearance of a "long" or "short" signal represents the resonance of multiple indicators, satisfying extremely stringent filtering conditions:

- 1. Vegas Channel Filtering:

- When going long, the price must be above the slow channel (576/676 EMA) and the fast channel (21/55 EMA).

- When shorting, the price must break below both the slow and fast channels.

- Interpretation: This ensures your trading direction is perfectly aligned with the medium- to long-term macro trend.

- 2. Alligator Line Confirmation:

- When going long, the price must be above the alligator lines (lips, teeth, jaws), and the alligator lines must be in a bullish alignment (opening upwards).

- When shorting, the opposite applies.

- Interpretation: This confirms that short-term momentum aligns with the long-term trend, avoiding hasty entry at the start or end of a trend.

- 3. OBV (On-Balance Volume) Filter:

- When going long, the OBV value must be above its own moving average (default 34 periods).

- When shorting, the OBV value must be below its moving average.

- Interpretation: OBV is a key indicator measuring fund inflows and outflows. This condition ensures that trading volume (funds) is supporting your trading direction.

- 4. ADX Trend Strength Filter:

- Whether going long or short, the ADX value must be greater than the set threshold (default 20).

- Interpretation: This is a crucial "insurance" layer. It helps filter out volatile market conditions with no clear direction, prone to repeated "misjudgments." We only act in markets with clear and strong trends.

Core Usage: Once a "long"/"short" signal appears, it represents a high-certainty trend-following trading opportunity. Due to the very strict nature of the signals, they appear infrequently, but each one deserves your close attention.

Module Three: Vegas Channel & Alligator Line (Trend Judgment Tool)

- Vegas Channel: Composed of two sets of EMAs.

- Slow Channel (576/676): Your "bull/bear dividing line." Above this line, only consider going long; below this line, only consider going short. It is your strategic compass.

- Fast Channel (21/55): Your "short-term momentum line." In an uptrend, price pullbacks to the vicinity of the fast channel are potential areas for adding to positions or entering.

- Alligator Line:

- Widening divergence: Indicates that a trend is underway.

- Convergence/Entanglement: Indicates the market is dormant or consolidating.

- Interpretation: Alligator lines allow you to visually see whether the market is in a "trending" or "consolidating" state. We primarily trade when the alligator lines widen.

Module Four: R/C Volume-Price Signals (Refined Entry/Warning Signals)

This is the system's "special forces," specifically designed to identify abnormal volume and price movements on key candlesticks. It is divided into the R series (Reversal) and the C series (Continuation).

- Prerequisites: All signals are based on trading volume. A signal's appearance must be accompanied by a significantly higher-than-average trading volume (increased volume). This indicates large capital participation at that price level, making the signal more reliable.

- R Series - Trend Reversal Signals (Warning/Opportunity):

- R1 (Core Reversal): In a downtrend, a sudden increase in volume on a bullish candlestick; or in an uptrend, an increase in volume on a bearish candlestick.

- Interpretation: This is the most basic reversal warning signal. It tells you that counter-trend forces are emerging, but it doesn't mean the trend will immediately reverse. Confirmation needs to be combined with other signals.

- R2 (Pattern Confirmation): In addition to R1, this candlestick must also be a well-defined Pin Bar (a bullish Pin Bar with a long lower shadow, or a bearish Pin Bar with a long upper shadow).

- Interpretation: This is a more reliable reversal signal. The Pin Bar pattern represents a strong rejection of the price after an attempt to break through; combined with increased volume, this indicates strong reversal momentum.

- R3 (Top Momentum): In addition to R2, the trading volume reaches a "massive" level (default is more than 4 times the average volume).

- Interpretation: This is the highest level reversal signal. It usually appears at the end of a trend, representing the extreme struggle and conversion of bullish and bearish forces, and is a potential sign of a "V-shaped reversal" or a deep V-bottom/top.

- C Series - Trend Continuation/Termination Signals:

- C0 (Trend Continuation): In a clear uptrend, a bearish Pin Bar (long upper shadow) with increased volume appears during a price pullback; or in a downtrend, a bullish Pin Bar (long lower shadow) with increased volume appears during a rebound.

- Interpretation: This is a classic "buy on pullback/sell on rebound" signal. It indicates that the pullback/rebound attempt to counterattack is quickly suppressed by the strong main trend, making it an excellent entry point for adding to positions or following the trend.

- CX (Exhaustion Signal): A C-series signal that appears when the price has moved far away from the slow Vegas Channel (default more than 5 times the ATR distance).

- Interpretation: This is an advanced use of the C-series. After a trend has run for a long time, market sentiment may be overly enthusiastic. The high-volume PinBar appearing at this time, while trend-following in form, is more likely to represent the exhaustion or "final frenzy" of the trend. This is an alert that the trend may be running out of momentum, and you should consider taking profits in batches rather than adding to your position.

Signal Priority: This indicator has been internally optimized: CX/R3 > R2 > C0 > R1. Higher-level signals will override lower-level signals, ensuring you see the most important information at the moment.

Module 5: Chandelier Exit - Dynamic Risk Management

This is a dynamic stop-loss system based on ATR (Average True Range).

- How it works:

- In an uptrend, it subtracts N times the ATR from the recent high, forming a stepped upward stop-loss line.

- In a downtrend, it adds N times the ATR from the recent low, forming a stepped downward stop-loss line.

- Core advantages: It automatically adjusts the stop-loss distance based on market volatility. During periods of high market volatility, the stop-loss widens, giving you more room; during periods of market stability, the stop-loss tightens, locking in profits more quickly.

- Usage:

- As an initial stop-loss: After entering a position, the stop-loss can be set outside the Chandelier line.

- As a trailing stop: The position is held as long as the price does not fall below (uptrend) or rise above (downtrend) the Chandelier line. This is a powerful tool for "letting profits run."

- As an auxiliary trend indicator: The direction of the chandelier line (upward/downward) also provides a concise short-term trend perspective.

Module Six: Candlestick Coloring

This feature is very intuitive; it colors candlesticks based on volume:

- High Volume (Orange): Volume exceeds twice the average volume.

- Huge Volume (Red): Volume exceeds four times the average volume.

- Usage: Helps you identify key candlesticks indicating significant market events at a glance, typically the start, acceleration, reversal, or exhaustion points of a trend.

Module Seven: ICT Market Structure

This is an advanced price behavior analysis tool based on ICT (Inner Circle Trader) theory, helping you understand the market's "skeleton."

- Core Concepts:

- Swing High/Low: Local tops and bottoms in market prices.

- BOS (Break of Structure): In an uptrend, the price creates a higher high than the previous swing high; in a downtrend, it creates a lower low.

- Interpretation: BOS (Bullish Oscillator) is a confirmation signal of trend continuation. Consecutive upward BOS indicate a healthy bullish trend, and vice versa.

- MSS (Market Structure Shift, also often called CHOCH): In an uptrend, the price fails to make a new high and instead falls below the previous valid swing low.

- Interpretation: MSS is the first and most important signal of a potential trend reversal. It indicates that market forces are shifting from bullish to bearish (or vice versa).

- Period Settings (Short/Intermediate/Long Term):

- Short Term: Based on the most minute 3-bar swing points, very sensitive, suitable for short-term traders to observe subtle changes.

- Intermediate Term (Recommended): Based on higher-level swing points formed from short-term swing points, filtering out some noise, suitable for day and swing traders.

- Long Term: Based on swing points formed from intermediate-term swing points, reflecting a longer-term structure, suitable for swing and long-term traders.

- Usage: Combine market structure with your trading signals. For example, in an uptrend (price above the Vegas Channel), each upward BOS confirms the health of the trend. If a C0 pullback signal appears at this point, it would be an excellent entry point. Conversely, if an MSS appears, even with a strong buy signal, caution is advised, as the trend may be reversing.

Module Eight: Information Panel

This is your "cockpit dashboard," consolidating all key information in one place, giving you a clear overview of the current market state:

- Main Trend Direction: The final trend judgment given by multiple indicators.

- Alligator Line Pattern: Shows whether the current trend is trending or consolidating.

- OBV Status: Whether funds are flowing in or out.

- ADX Status: Whether the trend is strong or weak.

- Chandelier Stop-Loss Direction: Short-term trend direction.

Lot Size Calculator - Gold🥇 Lot Size Calculator for Gold (XAU/USD)

Description:

A professional and accurate lot size calculator specifically designed for Gold (XAU/USD) trading. This indicator helps traders calculate the optimal position size based on account balance, risk percentage, and stop loss distance, ensuring proper risk management for every trade.

Key Features:

Accurate Gold Calculations - Properly accounts for Gold pip values ($10 per pip for standard 100oz lots)

Multi-Currency Support - Works with USD, EUR, and GBP account currencies

Flexible Contract Sizes - Supports Standard (100 oz), Mini (10 oz), and Micro (1 oz) lots

Customizable Decimal Places - Display lot sizes with 2-8 decimal precision (no rounding)

Clean Visual Design - Modern, professional info panel with gold-themed styling

Adjustable Display - Position panel anywhere on chart with customizable colors and sizes

Real-Time Calculations - Instantly updates as you adjust your risk parameters

How It Works:

The calculator uses the standard forex position sizing formula optimized for Gold:

Lot Size = Risk Amount / (Stop Loss in Pips × Pip Value Per Lot)

For Gold (XAU/USD):

Standard Lot (100 oz): 1 pip = $10

Mini Lot (10 oz): 1 pip = $1

Micro Lot (1 oz): 1 pip = $0.10

Settings:

Account Settings:

Account Balance: Your trading capital

Account Currency: USD, EUR, or GBP

Risk Percentage: How much to risk per trade (default: 2%)

Contract Size: 100 oz (Standard), 10 oz (Mini), or 1 oz (Micro)

Display Currency: Choose how to display risk amounts

Trade Settings:

Stop Loss: Your SL distance in pips

Display Settings:

Label Position: Top/Bottom, Left/Right, Middle Right

Label Size: Tiny to Huge

Decimal Places: 2-8 decimals

Custom Colors: Background, text, and accent colors

Perfect For:

Gold (XAU/USD) day traders and swing traders

Position sizing and risk management

Traders using fixed percentage risk models

Anyone trading Gold CFDs or spot markets

Scalpers to long-term Gold investors

What Makes This Different:

Unlike generic lot size calculators, this tool correctly calculates Gold's pip values based on contract size. Many calculators get this wrong, leading to incorrect position sizing. This indicator ensures you're always trading the right lot size for your risk tolerance.

Example Usage:

Account Balance: $10,000

Risk: 1% = $100

Stop Loss: 60 pips

Contract Size: 100 oz (Standard)

Result: 0.1667 lots (exact, no rounding)

Perfect for maintaining consistent risk management in your Gold trading strategy!

AI Scalping Signals# 🤖 AI-Powered Scalping Indicator - Ultra-Fast Trading Signals

## Overview

This advanced AI-driven **scalping indicator** is specifically engineered for high-frequency traders operating on smaller timeframes. Designed exclusively for **1-minute, 3-minute, and 5-minute charts**, this system combines multiple sophisticated technical analysis methods to identify rapid-fire, high-probability trade entries and exits. The AI algorithms analyze market momentum, micro-trend strength, and instant price dynamics in real-time, delivering lightning-fast BUY and SELL signals perfect for scalping strategies.

## Key Features

### ✨ AI-Enhanced Scalping Signal Generation

- **Machine Learning Integration**: Proprietary AI algorithms process multiple technical indicators simultaneously with millisecond precision to catch quick market moves

- **Smart Cross-Validation**: The AI system validates signals across multiple micro-conditions before generating alerts, perfect for fast-paced scalping

- **Adaptive Micro-Trend Analysis**: Intelligent momentum and trend detection optimized specifically for 1M, 3M, and 5M timeframes

- **Low-Latency Processing**: Designed for speed—signals generate instantly when conditions align for rapid trade execution

### 📊 Clean Visual Interface for Fast Trading

- **Crystal Clear Signals**: Easy-to-read BUY (green) and SELL (red) labels appear directly on your chart—no delay, no confusion

- **Background Confirmation**: Subtle background highlighting provides additional visual confirmation of scalping signals

- **No Chart Clutter**: The indicator focuses on signals only—no unnecessary lines or plots to distract from rapid price action and quick decision-making

- **Optimized for Speed**: Minimalist design allows you to spot and execute trades in seconds

### 🔔 Comprehensive Alert System for Scalpers

- **Real-Time Notifications**: Get instantly notified when AI-confirmed BUY or SELL signals are generated—critical for scalping success

- **Multi-Alert Options**: Separate alerts for buy signals, sell signals, or combined alerts for any scalping opportunity

- **Never Miss a Quick Move**: Set up alerts and let the AI monitor rapid market movements 24/7

- **Mobile-Friendly**: Receive alerts on your phone for on-the-go scalping

## How It Works

The indicator employs a sophisticated multi-layer analysis system optimized for scalping:

1. **Micro-Trend Analysis Layer**: AI algorithms analyze rapid trend shifts using advanced moving average techniques calibrated for small timeframes

2. **Momentum Spike Detection**: Smart momentum oscillators identify instant overbought and oversold conditions with scalping-level precision

3. **Price Action Validation**: Proprietary price cross-detection ensures signals align with actual market microstructure movements

4. **AI Flash Confirmation**: All conditions are processed through ultra-fast AI validation logic for immediate signal generation

### Signal Conditions

**🟢 BUY Signal (Long Scalp Entry)**

Generated when the AI system confirms:

- Bullish micro-trend alignment detected

- Price momentum shows instant strength above key thresholds

- AI-validated upward price breakout occurs on small timeframe

- Multiple technical confirmations align simultaneously for quick profit potential

**🔴 SELL Signal (Short Scalp Entry)**

Generated when the AI system confirms:

- Bearish micro-trend alignment detected

- Price momentum shows instant weakness below key thresholds

- AI-validated downward price breakdown occurs on small timeframe

- Multiple technical confirmations align simultaneously for quick profit potential

## Best Practices for Scalping

### Recommended Usage

- **⚡ Optimal Timeframes**: Specifically calibrated for **1-minute, 3-minute, and 5-minute charts** for maximum scalping performance

- **Markets**: Highly effective on forex pairs (especially majors), crypto (BTC, ETH), and high-liquidity stocks and indices

- **Session Focus**: Best results during high-volume trading sessions (London/NY overlap for forex, market open for stocks)

- **Quick Execution**: This is a scalping tool—execute trades immediately when signals appear

- **Risk Management**: Use tight stop-losses (5-15 pips for forex) and quick take-profits; scalping requires strict risk control

### Scalping Strategy Tips

- Execute trades instantly—scalping requires fast action within seconds of signal generation

- Use 1:1 or 1:2 risk-reward ratios for consistent scalping profits

- Monitor spreads and commissions—they matter significantly for scalpers

- Trade during high liquidity hours to ensure tight spreads and quick fills

- Consider trading multiple signals per session for accumulated gains

- Set mobile alerts to catch quick opportunities throughout the day

- Close positions quickly—don't let scalps turn into swing trades

- The background color change provides a split-second early warning system

## What Makes This Scalping Indicator Different?

Unlike traditional indicators designed for longer timeframes, this AI-powered scalping tool:

- ✅ **Built Exclusively for Scalping**: Optimized specifically for 1M, 3M, and 5M timeframes—not a generic indicator

- ✅ Combines multiple technical analysis methods with millisecond-precision AI processing

- ✅ Uses artificial intelligence to filter noise and validate only the fastest, cleanest scalping signals

- ✅ Eliminates the need to manually analyze multiple indicators during rapid market moves

- ✅ Provides clear, actionable signals with no interpretation required—critical for scalping speed